Technical Report 37

Rhonda Skaggs, Professor, Department of Agricultural Economics and Agricultural Business

College of Agriculture, Consumer and Environmental Sciences New Mexico State University. (Print Friendly PDF)

Table of Contents

Introduction

Megatrends No. 1 and No. 2

Megatrends No. 3 and No. 4

Megatrends No. 5 and No. 6

Megatrend No. 7

Megatrends No. 8 and No. 9

References

Introduction

For several years, I have taught about food and agricultural policies, agricultural structure, and the future of agriculture in the Department of Agricultural Economics and Agricultural Business at New Mexico State University (NMSU). One of my biggest challenges has been to get students to see agriculture from a broad, sectorwide perspective. I urge them to think economically about agriculture and to examine critically their perceptions of the food and agricultural system in the United States. They are encouraged to become more aware of the history, current status, and future of U.S. agriculture, the influence of international trade on the sector, and their own role within the global food and agricultural economy.

In every class I’ve taught, students have had the same questions and the same degree of puzzlement about food and agricultural issues. This document is a compilation of many of their questions or comments, and is, thus, presented in a question and answer format. The subjects of the questions include agricultural prices, the structure of agriculture, food demand, and international issues. The questions and answers are organized by what I call megatrends or powerful forces and trends confronting the agricultural economies in both New Mexico and the United States.

Over the past several years, I also have given numerous presentations to nonstudent audiences throughout New Mexico about the trends and issues discussed here. These audiences have included agricultural producer and agribusiness organizations, community development forums, and non-agricultural groups. The reactions and questions I’ve encountered in these settings have been similar to those of the university students. Thus, the objective of this report is to formally organize the information I’ve given to all the groups I’ve spoken to–university and non-university. I hope this report will contribute in some small way to the current debate over the future of agriculture in New Mexico.

After discussion of several megatrends, this document concludes with Internet Web sites where additional information can be located.

Megatrends No. 1 and No. 2

Real prices for agricultural commodities will continue to go down, and technology will continue to reduce per-unit costs of production.

What is a “real” price?

Changes in the value of money (inflation or deflation) affect the nominal or market prices of all goods and services. Real prices are calculated such that the effects of inflation are removed. While a product’s market price may move up or down depending on year-to-year changes in supply, demand, and the value of money, a real price for a product is a true measure of scarcity, value, and relative purchasing power over time.

What has happened to real agricultural prices during the last century?

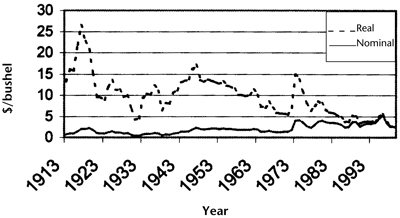

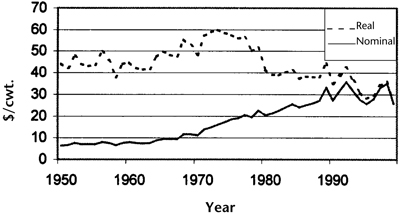

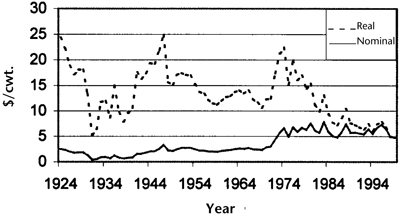

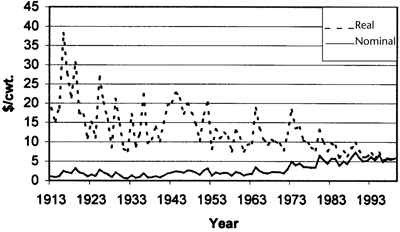

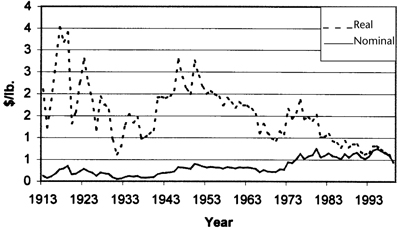

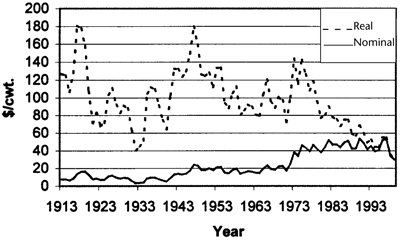

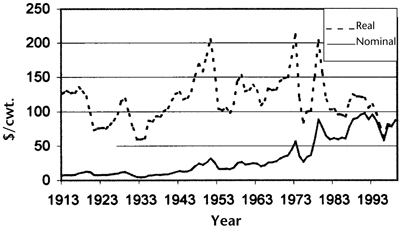

Real prices for most agricultural commodities have decreased during the last century. Real producer prices for selected crop and livestock products are shown (figs. 1-7). Real price movements vary among the commodities, with beef calves showing the flattest downward trend. These variations are largely due to differences in productivity gains during the years presented. Some of the greatest gains in productivity have been made in the hog industry, thus, real hog prices show one of the sharpest downward movements since the 1940s. Productivity gains in the beef industry have not been as great, resulting in more real price stability over time. Year-to-year market price volatility has created severe hardship for many producers and forced some out of business in past decades, but long-term trends in real prices have been the dominant force in shaping the structure of U.S. agriculture during the last century.

Figure 1. Real and nominal prices of wheat, 1913–1999 (1999 = 100). Source: U.S. Department of Agriculture.

Figure 2. Real and nominal prices of tomatoes, 1950–1999 (1999 = 100). Source: U.S. Department of Agriculture.

Figure 3. Real and nominal prices of soybeans, 1924–1999 (1999 = 100). Source: U.S. Department of Agriculture.

Figure 4. Real and nominal prices of upland cotton, 1913–1999 (1999 = 100). Source: U.S. Department of Agriculture.

Figure 5. Real and nominal prices of potatoes, 1913–1999 (1999 = 100). Source: U.S. Department of Agriculture.

Figure 6. Real and nominal prices of hogs, 1913–1999 (1999 = 100). Source: U.S. Department of Agriculture.

Figure 7. Real and nominal prices of calves, 1913–1999 (1999 = 100). Source: U.S. Department of Agriculture.

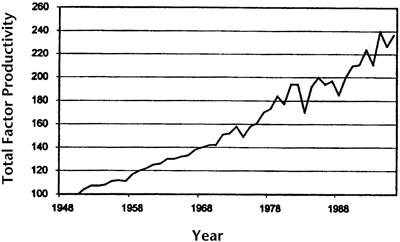

Figure 8. Growth in the U.S. agricultural productivity, 1948–1996 (1948 = 100). Source: U.S. Department of Agriculture–Economic Research Service.

Why have real agricultural prices decreased?

Real prices for agricultural commodities have decreased because supplies have grown faster than demand. Agricultural commodity output increases because of two forces: increased inputs (more land, people, resources) and increased productivity (the rate of output to input).

In the 1800s and the early part of the 20th century, total U.S. farm output increased primarily because of an increase in the total amount of land dedicated to agricultural production. Settlers pushed back the frontier, farmed new lands, developed irrigation infrastructure in the West, and added more farms and farmland. Technological advances were occurring during this period, but they were a less important contributor to total output increases.

Since 1920, except for irrigation development in a few Western states, total agricultural output has resulted from technological advances that have dramatically increased productivity. Figure 8 shows agricultural productivity in the United States since 1948. Total input use by U.S. agriculture has decreased, while total output has increased greatly. Capital inputs have been substituted for land and human labor. The quality of both human and capital inputs also has increased.

What does technology do to agricultural production?

New technologies expand output and reduce per unit production costs. U.S. farmers and ranchers historically have produced for markets in which no one producer has any perceptible influence on the product’s price. Each producer is such a small part of the total market that individual changes in output will not affect the aggregate market price. Such producers are called price takers.

Over the last century, as new agricultural technologies were introduced to producers, a small number started using the technologies (hybrid seeds, tractors, chemical fertilizers) early in the game. The new inputs reduced per unit costs of production and increased the output of a few early adopting producers. Because the neigh technology users were a relatively small part of the market, they had no effect on the market price. For a short time, their net returns were higher than nonadopting producers. However, information about the new technologies spread, and other producers started using them. At some point, widespread adoption of new technologies resulted (and continues to result) in increases in total supplies that lower prices for all producers. The continual introduction and adoption of new agricultural technologies is often referred to as the “technological treadmill.” Over the last century, millions of farmers were unable to stay on the treadmill and became part of a huge exodus out of agriculture to other sectors of the economy. Technologies that increase output and reduce costs in agriculture released human resources for employment in other professions. The technologies have driven down raw material costs for the rest of the economy, including all food and fiber consumers. The technologies also have made it possible to produce more output on less land.

Decreasing real prices are evidence of a highly successful, advancing agricultural sector, although some human resource adjustments, such as migrating to the city, have not been without pain.

How can supply increase faster than demand when there are millions of hungry people all over the world?

Hungry people throughout the world often don’t get the nutrition they need because their countries suffer continual political upheaval or war. Normal agricultural production and food distribution systems don’t function well under unstable political or social conditions.

Demand for food worldwide is growing, but much of that demand is not “effective.” When demand is effective, consumers have the ability to buy food in the marketplace at a price producers can afford. Given the extremely low per capita incomes in many developing countries, many people do not have the financial ability to get all the food they need, or to improve the quality of the food they consume. Also, in countries that are not open to trade, food shortages and hunger can result.

The supply and demand relationship that has led to decreasing real prices for agricultural commodities is a function of effective demand. Effective demand worldwide will increase only with economic growth and higher per capita incomes in poor countries.

Where do agricultural technologies come from?

The first significant advances in agricultural technologies were the result of private inventors, such as John Deere and Cyrus McCormick. In the late 1800s, the federal government assumed a prominent role in developing technologies that increase productivity. Much of this publicly funded research and development has been conducted in colleges of agriculture at institutions, such as NMSU. The current trend is toward fewer public funds for research aimed at increasing output, and increased private sector research. Many of the more recent advances in agricultural technologies have been the result of private sector investments or public-private partnerships.

Won’t population growth worldwide eventually lead to increasing real prices for food?

Total world population is approximately six billion. The global population is expected to start leveling off at about 8.9 billion in 2050, eventually stabilizing at 11-12 billion. Clearly, there will be a growing demand for food in the future. And if incomes increase in low- and middle-income countries, consumers there will want to consume not only more food, but higher quality foods. Currently, there appears to be no shortage of output-increasing technologies in agriculture. However, “high-yield” agriculture is strongly criticized by proponents of more traditional food producing technologies and systems.

Globally, about 2,700 calories are available per person per day. This amount exceeds minimum nutritional requirements. Yet almost a billion people do not have access to adequate food supplies because of persistent poverty, economic instability, economic stagnation or decline.

Population growth in high-income countries and other areas (including former Soviet Republics) is extremely low and is not likely to increase. Significant growth in food demand due to population growth will not occur in many countries. Aging populations will dominate several countries in coming decades, and will actually lead to reductions in aggregate food consumption. Furthermore, the markets for food are effectively saturated in the wealthiest nations of the world (United States, Japan, Western Europe).

At this point, there is no evidence that real agricultural prices will reverse their long-term downward trend.

What have farmers done as a result of the decreasing real prices offered for their products?

There have been four basic responses by the farm sector to decreases in real prices. First, many farmers and farmworkers left the farm sector. This choice was most prevalent in the 1950s and 1960s, when millions migrated to urban-industrial employment and living. Second, many who stayed in agriculture and didn’t fall off the treadmill bought or rented their exiting neighbors’ farms. They increased their scale of operation, thus improving their ability to generate acceptable net farm incomes in the face of the chronic decreasing net returns resulting from the treadmill effect. The trends of steadily decreasing farm numbers and total farm population, along with increasing average farm size, have characterized U.S. agriculture since the 1920s.

A third response to decreasing real prices has been for farmers to obtain off-farm employment in order to achieve acceptable total household incomes. For the majority of U.S. farms, income earned off the farm subsidizes farm or rural lifestyles, and involvement in agriculture is primarily a consumptive activity. Since the mid-1970s, off-farm income earned by the farm sector has been greater than total net farm income.

The most recent response has been for producers to develop strategies that enable them to avoid being price takers. These farmers and ranchers have developed niche markets for their food and fiber products, based on real or imputed differences between them and the rest of the market. Organic production, animal welfare friendly production, and brand names tied to individual farms are means by which some producers have been able to escape the trend of decreasing real prices. Some producers also have learned to use various price risk management strategies, such as futures and option contracts, as well as vertical coordination and integration.

Can’t the government do something to keep real prices from falling?

Falling real prices throughout the 20th century led to demands by the farm sector for government help. Billions of federal dollars have flowed into agriculture since the 1930s. These subsidies have helped to maintain the long-run situation of supply increasing faster than demand, thus, contributing to real price decreases for many agricultural products. Simultaneously, throughout the last century, the government has promoted the development of output-increasing agricultural technologies. As described above, the entire economy has benefited as a result of the fall in real prices. It is unlikely that the U.S. government could or would ever create a situation of stable or increasing real prices for food. It is unlikely that there would ever be a widespread desire to put the agricultural technology genie back into the bottle! The farms currently producing the majority of U.S. agricultural output, food manufacturers, and consumers would not support such a policy. Government payments to agricultural producers no longer attempt to keep prices up and currently are direct income subsidies.

Megatrends No. 3 and No. 4

Demand for food in the United States will not grow significantly in the future, and the farm share of the retail food dollar will decline.

Why won’t demand for food in the United States grow?

The U.S. population (and that of other wealthy nations) is very affluent and very well fed. Demand for food in these countries is extremely income inelastic, meaning that increases in incomes will not result in significant increases in food demand or consumption. The mix of foods that people consume may change slightly, but overall quantity increases are unlikely. Demand for food also is price inelastic, meaning that consumers don’t change their food buying habits very much as a result of price increases or decreases.

Food demand in the United States and other wealthy countries is saturated. One of the greatest public health issues facing the United States at the current time is overnutrition, rather than undernutrition. Excess consumption of calories, especially calories from fatty and sweetened products, is a cause of obesity and linked to numerous health disorders, including diabetes, heart disease, and cancer. The U.S. population also is aging and growing very slowly. Farm level food demand in the United States is probably growing not more than 1% per year.

What does this mean for U.S. farmers?

The future of much of U.S. agriculture depends on international markets. Without trade (and trade growth), the United States will need a lot fewer farmers (and other resources devoted to agricultural production) in the future.

But people will always need to eat, so food demand will always be there, won’t it?

Yes, food demand will remain strong in the United States. However, the nature of what people consume will continue to evolve. An increasingly affluent society has a growing demand for what are called food “services.” The share of food dollars spent on food away from home is now almost 50% of American’s total expenditures on food. In buying food at restaurants, consumers are buying dining experiences, convenience, and many other services. Likewise, recent years have seen the development of numerous convenience foods for consumption at home. Many supermarkets now offer entire meals for consumption at home, along with an amazing variety of precooked or semiprepared items. Busy, time-pressed consumers appear very willing to pay the extra costs for more convenient supermarket items and restaurant meals. Consequently, the farmers’ share of retail food expenditures is at an all-time low of approximately 20%.

Isn’t it unfair that farmers and ranchers receive such a small percentage of what consumers pay for food?

Whether or not this situation is “unfair” is a value judgment, and one that completely ignores the reality of what happens to food between the farm gate and the consumer’s plate. Labor, packaging, transportation, advertising, energy, taxes, and many other costs are incurred in transforming raw agricultural commodities into items desired by consumers. And as stated above, consumers now want more from their food products than the food. If Americans baked their own bread or ground their own sausage, the wheat and hog farmers’ shares of the value of the final consumer products would be a lot higher. But it is extremely unlikely that very many Americans want to engage in that level of food processing. Thus, as a general rule, the more processing and/or value adding done to a product, the smaller the percent of retail value farmers receive.

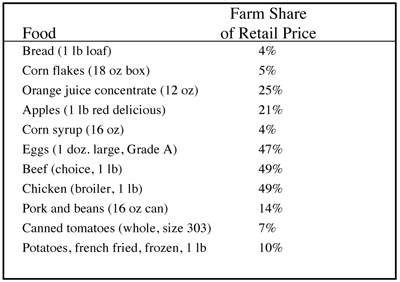

What are the farm shares for some individual food products?

Figure 9 below shows the farm share of the retail prices for selected food items in the United States. The farmer share of the retail prices is generally higher for less processed food items.

Figure 9. Farm shares for selected food items in the United States. Source: U.S. Department of Agriculture–Economic Research Service.

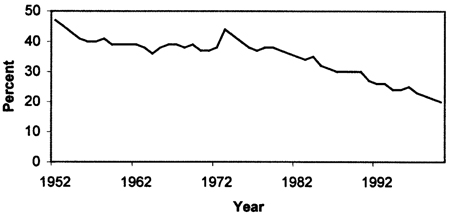

What will happen to the farm share of the retail food dollar in the future?

The farm share of the retail food dollar will continue to decrease, as Americans consume more food away from home and more heavily processed items. Figure 10 shows the farm value share of retail food expenditures during the last several decades.

Figure 10. Farm value share of retail price, 1952–99. Source: U.S. Department of Agriculture–Economic Research Service.

Can’t the government do something to raise the farm share of retail food expenditures?

The proper role of the government in this capacity is to ensure that producers of raw agricultural commodities are not subject to monopsony or oligopsony buying practices (situations where one or a small number of buyers use their unequal market power to pay lower prices). Any government attempt to increase the farm share of retail food expenditures by increasing commodity prices could increase slightly the raw material costs of food manufacturers, but would not necessarily increase the farm share of the retail dollar. However, under conditions of liberalized trade, any attempt to fix commodity prices higher than they would be under competitive market conditions would lead food manufacturers to look for alternative sources for their raw materials. These alternative sources could include vertically integrated production by the food processors themselves, or by processors in other countries.

In conclusion, food demand at the farm level in the United States will not grow significantly in the future, although the demand for processing and marketing services will increase with economic growth overall. Given current social and economic trends, the farm share of the retail food dollar will likely decrease in the future.

Megatrends No. 5 and No. 6

The importance of international trade to the U.S. food and agricultural system will increase, and U.S. consumers will eat more imported food.

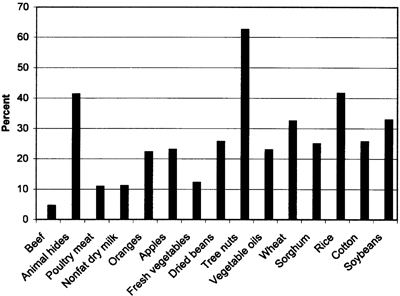

How important is trade to U.S. agriculture?

Overall, trade is very important to U.S. agriculture. The importance of trade to selected agricultural products is shown (fig. 11). Agricultural product exports have accounted for 20-30% of total U.S. farm income in recent years. As explained above, the U.S. market for food is quite saturated, almost everyone is well-fed, and quite a few of us are overfed. If every U.S. citizen were able to double their incomes over the next year, they still would not consume more food. Without international trade, the U.S. would need a lot less production, fewer farmers, and fewer resources devoted to agricultural production. Unless we want to shrink the size of the entire U.S. food and agricultural system (farm production, related agribusinesses, and food processing), international trade is absolutely necessary.

Figure 11. Export share of U.S. agricultural production, 1999. Source: U.S. Department of Agriculture–Economic Research Service.

But I’ve heard that some U.S. producers are being hurt by agricultural imports!

While trade is essential to U.S. agriculture in the aggregate, this does not mean that some agricultural products will not be negatively affected as a result of having to compete with imported products. International trade encourages countries to produce and trade commodities for which they have some comparative advantage. The comparative advantage can be related to a nation’s natural resource base, development of and investments in technology over time, and the quality and quantity of human resources (labor costs). Countries also tend to have international trade advantages for goods or services for which they have a relatively large domestic market.

As the world’s agricultural economy grows and becomes increasingly integrated through trade, nations will tend to specialize in the production of certain products. The United States currently has an advantage in the production of capital-intensive, land-extensive, and low-labor input crops that can be mechanically harvested, such as corn and soybeans. The United States is a much less competitive and higher cost producer of labor-intensive vegetable crops, such as chile peppers. U.S. imports of fruits and vegetables have grown in recent years, as consumers reap the benefits of year-round access to high-quality, relatively inexpensive grapes, peaches, melons, and many other imported foods. In the long-run, the United States will import more of these goods, and produce less here. Simultaneously, our producers of corn and soybeans (and other goods) will have to work hard to stay on the technological treadmill in order to assure that their competitive position is not eroded.

What is the long-run outlook for global agricultural markets?

As a result of increasingly free international trade, agricultural producers worldwide are in a race to become more efficient, reduce per unit production costs, capture market shares, and keep up with progressively lower real prices. The greatest beneficiaries are all consumers and raw material users. Some people in U.S. agriculture think it would be desirable for trade to be one-sided, with the United States taking advantage of growing exports while simultaneously closing our market to food imports from abroad. However, that situation is not a viable solution to adjustments that must continue to be made by the U.S. farm sector. As with technology, putting the trade genie into a bottle is both undesirable and unlikely to happen. What will happen with trade is that U.S. consumers will eat more fruits and vegetables of foreign origin, while consumers in other countries will eat more American corn-based products, processed foods, meats, and vegetable oil.

Megatrend No. 7

The structure of U.S. agriculture will continue to become more “dualistic.”

What is the “dual farm structure?”

The phrase “dual farm structure” is used to describe the current structure of U.S. agriculture, where 18% of farms produce more than 87% of the output, and 82% of farms produce approximately 13% of the output. Farms with more than $100,000 in sales traditionally have been considered “commercial” farms that are capable of generating positive net farm incomes after production expenses. Net farm income is generally one third of gross farm sales. The 18% of U.S. farms that produce 87% of the value of U.S. agricultural output are farms with sales over $100,000.

A new farm classification system recently was developed by U.S. Department of Agriculture’s Economic Research Service. The system uses a $250,000 gross sales cutoff, with small farms having sales less than this amount. The system includes five subcategories within the small farm group, based on total farm resources, nature of off-farm income sources, and total sales volume. Nationally, farms with less than $250,000 in sales make up 92% of all farms and account for 28% of the value of all production.

What is the definition of a “farm?”

A farm is any place from which $1,000 or more of agricultural products were produced and sold, or normally would have been sold, in a given year. This is the definition that is used by the United States Census of Agriculture to enumerate the farm sector. In 1997, the United States had 1.9 million farms. The use of the word “farm” includes places that produce and sell all varieties of crops or plant-based commodities, and places that produce and sell all types of livestock. The term “farm sector” thus includes agricultural operations that produce only livestock commodities. Furthermore, one shouldn’t get too hung up on the use of the term “ranch,” because in California, avocadoes and almonds are produced on avocado and almond ranches.

How do farms in the lower sales categories survive?

Fifty percent of what we call “farms” (using the Census of Agriculture definition) sell less than $10,000 worth of agricultural commodities annually and almost 75% of “farms” sell less than $50,000 worth of goods yearly. Using the rule of thumb that $1 in sales generates about 33 cents in net farm income, most of these farms must have extremely low net farm incomes! Actually, the 1.4 million farms in these lower sales categories tend to have chronic negative net farm incomes. Many rural households engage in commodity production, which allows them to reach the $1,000 annual sales threshold criteria to be called a farm for census purposes, but have no intention of earning a living from farming. Many of these people have rural residence lifestyles, and crop or livestock production is classified more properly as a consumptive activity.

The agricultural operations in the lower sales categories rely on off-farm jobs, retirement or social security payments, or other nonfarm income sources. Their rural residences and agricultural land are an investment, a legacy, or a lifestyle choice. In 1999, the national average household income for farms with annual sales of less than $50,000 was $62,925, while their farm earnings were negative $3,786.

Throughout the United States, there are some farm families living in extreme poverty, but this is usually the result of limited educational opportunities and little or no off-farm employment in their areas.

What has created the dual farm structure?The dual farm structure is partially the result of the technology treadmill described above. Technologies that increase output and reduce per-unit costs have led to larger farming operations because of the need for higher net farm incomes. With decreasing per-unit returns, producers have had to increase the scale of their operations or obtain off-farm employment to achieve acceptable household incomes. This has created one end of the dual farm spectrum.

The largest group of small farms (using the new USDA system) consists of rural residence or lifestyle farms. In recent years, the number of small farms (with annual sales less than $10,000) has grown in many regions of the United States (including New Mexico). People are making lifestyle choices that include smallscale commodity production, and as stated above, there appears to be a strong willingness to subsidize the farm lifestyle with off-farm income. Thus, the small-farm end of the dual farm spectrum continues to expand.

What is the future of agriculture structure in the United States?

Middle-sized farms are defined in a variety of ways. These are farms that have annual sales less than $250,000 (probably much less) and are operated by individuals who are attempting or would prefer to earn 100% of their income from their farm operations. However, they may have off-farm jobs in order to maintain acceptable and stable household incomes. They may be unable or unwilling to make the investments necessary to continue staying on the technological treadmill. This type of farm is sometimes referred to as the “disappearing middle,” and there are relatively few of these farms left. Their numbers will become smaller in the future, while the two extreme size categories (very small and very large sales) will continue growing, with most growth in the smallest sizes. More food and fiber will be produced on fewer large farms, but the total number of farms will be dominated by the smallest operations.

Megatrends No. 8 and No. 9

The environmental effects of agriculture will become increasingly important to society, and agricultural multifunctionality will be highly valued in some regions of the country.

Why does it seem like everyone wants to beat up on agriculture all of the time?

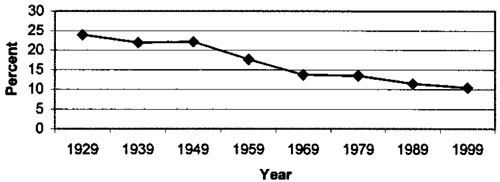

The United States is a very affluent country. The food needs of this country have been met. Although pockets of hunger exist, they are not due to food shortages. A household with an annual income of $40,000 spends approximately 13.7% of its after-tax income on food (fig. 12). The share of income spent on food products has changed during the last 70 years. A household with $70,000 in annual income spends less than 9% of its after-tax income on food. These expenditures include purchases of convenience food items and restaurant meals. As stated above, the farm share of the retail food dollar is 20%. Thus, the $40,000 income household is spending less than 3% of its after-tax income on the raw agricultural commodities that have been transformed into retail food products. For the higher income household, this amount is less than 2%.

Figure 12. Proportion of income spent on food, 1929–1999. Source: U.S. Department of Agriculture–Economic Research Service.

Our nation has been going through a period of unprecedented economic expansion and income growth. Our overall affluence and wealth are unmatched throughout the world. As people become increasingly affluent, their desire to consume more food diminishes, while their desire for other goods and services increases. These goods and services can include better and bigger housing; entertainment; personal services; electronic devices; and thousands of other items. An affluent population also will have an increased demand for what are generically called “environmental amenities.” A population that is no longer worried about food availability has the opportunity to be concerned about clean air and water, open space preservation, conservation, wilderness, and the environmental impacts of modern agriculture.

As more and more people disconnect from agriculture, including their own agricultural roots, and as food shortages fall further into the past, there will be a growing belief that food will always be in ample supply and that farming is an environmental problem. Hungry people usually don’t blame farmers for environmental damage. However, many affluent consumers appear to disconnect food at the restaurant and supermarket from the farm source or production process.

One of the consequences of affluence, as described above, has been pressure to change many traditional crop and livestock practices, and regulate large-scale industrial production, such as confined animal feeding. This has led to increased government monitoring and, in some instances, civil and criminal penalties for production practices that result in what are now defined as environmental crimes (air and water pollution, wetland destruction, pest eradication).

Why can’t everyone accept that farmers and ranchers are good stewards of the natural environment?

Belief systems often conflict when agricultural producers and environmentalists clash. At their extremes, one belief system holds that production agriculture can do no wrong and that the resource stewardship practiced by farmers and ranchers should be beyond reproach. In its most extreme form, the other belief system holds that the only desirable state for the natural world is pristine and untouched by human influence. Most of the population is somewhere in the middle of these two extreme beliefs.

If agricultural interests continue to deny that crop and livestock production can and have adversely impacted the natural environment, then they will be on the losing end of our nation’s cultural and political evolution. This evolution results from more than 200 years of economic growth, development, and diversification. It is a natural outcome of our economic transformation from an agrarian nation to an industrial one, and more recently into a post-industrial society. To expect that the farm sector can fight and prevail in repeated controversies over the environmental impacts of commodity production is naive at best. The majority of the food consuming public may not know much about where their food comes from, but just like with pornography—they know environmental degradation when they see it! When farm and ranch interests continue to insist that agriculture is environmentally benign, they look venal or foolish to the general public. Again, it is a socioeconomic reality that as incomes increase, demand for environmental amenities increases. Denial and attempts to work against that natural development have the potential to increase pressure for regulation and penalties for socially undesirable food and fiber production practices.

Why isn’t agriculture valued as much as it used to be?

Throughout most of the history of the United States, great emphasis was placed on increasing agricultural output. The history of mankind has been largely a battle against food scarcity, and the United States has long been a haven for people fleeing hunger and deprivation in their native countries. In the United States, we have placed great value on work, production, and productivity as a means for self-improvement and advancement of the nation. We were “productivists” in our view of the world. As a result, food scarcity in the United States is no longer a serious national concern. Consequently, some observers have called this latest stage in the development of our nation’s agriculture (and other industries as well) a “post-productivist” era.

We are in an era when the negative aspects of production (especially environmental costs) are noticed by the affluent public. The public also is less likely to believe that production, simply for the sake of production, is a good thing. The public appears less likely to support surplus production at all costs. However, in the United States (and in Western Europe), society seems to have retained some warm or nostalgic feelings toward traditional production agriculture or the pastoral way of life (unless they believe modern production methods are causing environmental damage). Many urban residents, only one or two generations removed from the farm, continue to believe rural areas and lifestyles are repositories of desirable social or moral values.

What are the other outputs or benefits of agriculture?

Another result of evolution to economic affluence and post-productivism is the increased recognition of agriculture’s “multifunctionality.” Multifunctionality refers to the fact that while agriculture has a food (and fiber) function, it also has other functions for society overall. Clearly, the food function is what feeds us. The nonfood functions include production agriculture’s contributions to the viability of rural economies and jobs, the provision of open space in many urban or rapidly urbanizing areas, and wildlife habitat and water development (in areas where agriculture has improved them). A multifunctional, local agricultural production system also may be an important part of a region’s cultural, historical, or social heritage. The phrase “landscape amenity” often is applied to describe agricultural open space or production areas that are aesthetically pleasing to casual observers.

The technological treadmill is leading to a situation where the entire United States (and many other nations throughout the world) probably could be fed with 100,000 farms or less. Liberalized trade is making it possible to have inexpensive, year-round access to high-quality fresh fruits and vegetables. In many parts of the United States, the dual-farm structure and large-scale industrial agricultural production methods are leading to a very clear distinction between farms that feed us and farms that are pleasant to look at, drive by, and live near. Many communities throughout the United States are grappling with how to preserve traditional agricultural character and heritage in the face of rapid population growth, economic diversification, competition for land and water resources, and the forces described throughout this paper.

How do farms vary in their food and nonfood functions?

The food function (the agricultural output) is linked to the nonfood function, and changes or differences in the quantity or nature of food output will affect the output of nonfood services. For example, a 5,000-cow, drylot dairy produces much more milk than a 50-cow dairy, but the landscape amenity value of an industrialized dairy operation is not the same as the small dairy farm. The commercial market value of the large farm’s production is many times that of the small dairy farm, but so are many negative outputs (smell, wastewater, manure). And while there is no market for the agricultural open space, picturesque vistas, and bucolic landscapes associated with the small farm, society appears to value them. The relative scarcity of these nonfood services has led to a growing interest in holding onto them in many communities. As discussed above, America’s small farms are not contributing very much toward total agricultural output. For many of these farms, the value to society of their nonfood function is likely to be much greater than the value of their food function!

How does multifunctionality relate to international agricultural trade and government subsidies to agriculture?

At the international level, the United States has taken the position that our trading partners cannot close their markets to our agricultural products in the interest of preserving their own multifunctional agricultural systems. Likewise, the United States will not close its markets because of concerns for the structure of our own agricultural system. The official U.S. policy is that high levels of market-distorting, agricultural subsidies in wealthy countries are not justified just because the nonfood benefits of agriculture are held in high esteem.

It is unlikely that the U.S. government will ever use trade policy or direct government intervention in order to “preserve” an ideal type of agricultural operation. Past attempts to target government subsidies to small- and medium-sized farms have not prevented the dual-farm structure from emerging. And even if more subsidies are paid to agricultural producers, the two ends of the dual-farm structure will continue to become further apart in what, how, and how much they produce. The concept of targeting government subsidies to a specific size or type of farm is politically popular and will continue to be promoted by family farm advocates, members of Congress, and others. However, the forces that have created the dual-farm situation are so powerful that targeted subsidies will have no effect on the structure of U.S. agriculture in the long run. U.S. farms and ranches will continue to show great variability in the relative importance of their food and nonfood functions, regardless of what happens with international trade or government subsidies.

How will multifunctionality be dealt with in the future?

In the future, efforts to preserve or maintain local agriculture will be undertaken primarily at the local or state levels. This will occur not because these systems are important to the national or even regional food supplies, but rather, because their nonfood function or spillover benefits are valued by nearby residents. These benefits include wildlife habitat, agricultural open space, a diverse rural economy, support to other industries (tourism), preservation of local heritage and other positive contributions to the natural environment . Policies that would help sustain local agricultural systems (and which are not considered to be trade-distorting) include purchasing or transferring development rights from agricultural lands, improving rural infrastructure and educational systems, and creating nonfarm jobs in rural communities. Most small farms will continue to be supported by off-farm income in the future. In many regions, preserving local agriculture will be a function of the availability of off-farm jobs and not necessarily related to any community interest.

One nonlocal aspect of agricultural multifunctionality that is gaining both domestic and international interest involves carbon sequestration by farmland. The 1997 Kyoto Protocol commits industrialized nations to reduce the buildup of carbon dioxide in the atmosphere in order to reduce global warming. Research is underway to evaluate the carbon capturing potential of U.S. cropland and how it varies with different farming practices. In order to encourage farmers to create conditions for high carbon sequestration levels, federal government involvement would be necessary, and likely involve some combination of regulation and subsidy.

References

Much of the information presented here was developed using resources provided by the USDA’s Economic Research Service (ERS). The USDA’s World Wide Web sites (especially that of the ERS) are easily accessible and provide a wealth of information about the U.S. food and agricultural sector, international trade, and agriculture in other countries. Several USDA Web sites are listed below.

United States Department of Agriculture–Economic Research Service. World Wide Web site: http://www.ers.usda.gov. This site provides analysis and data for many aspects of the U.S. food and agriculture sector, trade, and international agriculture.

United States Department of Agriculture–National Agricultural Statistics Service. World Wide Web site: http://www.nass.usda.gov. This site includes the Census of Agriculture (conducted every five years), and other data publications.

United States Department of Agriculture–Natural Resources Conservation Service. World Wide Web site: http://www.nrcs.usda.gov. This site provides information about agriculture, natural resources, and related government programs.

United States Department of Agriculture–Farm Service Agency. World Wide Web site: http://www.fsa.usda.gov. This site gives information about federal government programs that provide financial assistance to crop and livestock producers.

United States Department of Agriculture–Foreign Agriculture Service. World Wide Web site: http://www.fas.usda.gov. This site provides information about international trade in food and agricultural products, status of foreign markets, assistance for exporters, and international food aid.

United States Department of Agriculture. World Wide Web site: http://www.usda.gov. This is the primary Web site for the USDA, and includes links to all USDA agencies, including those listed above.

To find more resources for your business, home, or family, visit the College of Agricultural, Consumer and Environmental Sciences on the World Wide Web at aces.nmsu.edu.

Contents of publications may be freely reproduced for educational purposes. All other rights reserved. For permission to use publications for other purposes, contact pubs@nmsu.edu or the authors listed on the publication.

New Mexico State University is an equal opportunity/affirmative action employer and educator. NMSU and the U.S. Department of Agriculture cooperating.

Printed and electronically distributed November 2001, Las Cruces, NM.