Crop and Livestock Enterprise Budgets

What Are They and Why Do Producers Need Them?

Guide Z-119

Pilja Vitale, Jason Banegas, Madhav Regmi, Jay Lillywhite, Don Blayney, Michael Patrick1

College of Agricultural, Consumer and Environmental Sciences, New Mexico State University

Authors: Respectively, Extension Economist, Department of Extension Economics (EE); Extension Economist, EE; Assistant Professor, Department of Agricultural Economics and Agriculture Business (AEAB); Assistant Dean, Economic & Rural Development; Professor, AEAB; and Extension Specialist, EE, all from New Mexico State University. (Print-friendly PDF)

Chile Field, Deming, NM. 2020. (NMSU photo by Josh Bachman)

WHAT IS AN ENTERPRISE BUDGET?

An enterprise budget has been defined as “the basic building block of costs and returns of growing crops or raising livestock” by the New Mexico State University (NMSU) Cooperative Extension Service (NMSU, 2011). Enterprise budgets generally represent typical farming or ranching situations for a specific region. NMSU’s enterprise budgets are associated with a particular county within the state.

Each enterprise budget represents only one crop or livestock production activity and is calculated on the same per unit basis, such as per acre, so producers can easily compare multiple enterprises they may be operating. For example, a producer could grow wheat and sorghum so a budget for each crop can be developed. Enterprise budgets typically include detailed listings of the physical resources and inputs required for production, such as land, labor, fertilizer, fuel, or machinery, and the costs of those inputs and resources.

THE NEED FOR BUDGETS

Producers need to be able to estimate returns and costs associated with their farming and ranching operations. Enterprise budgets allow them to estimate potential returns and the money they will need to pay for inputs required to grow their crops and raise their livestock. The difference between revenues and costs can be used to approximate the net returns that a producer might expect for a particular enterprise. To producers, it is better to estimate returns and costs before planting their crops. In 1907, NMSU had already recognized the need for the budget by introducing a course entitled “Farm Accounts,” which stated that “a producer must know whether the producer is losing or gaining money as a result of his/her operations, not only as a whole but each crop and herd or individual of that herd must be made to answer searching questions of profit or loss.”

WHY ARE ENTERPRISE BUDGETS IMPORTANT?

Knowing Costs and Returns

A detailed accounting of costs and returns allows a producer the opportunity to identify potential areas that need additional management consideration. For example, on the revenue side, an enterprise budget could be used to identify prices or yields needed to meet a targeted net return, e.g., “break-even.” Alternatively, on the cost side, the budget can allow the producer to identify inputs where costs should be more carefully examined.

Farm Planning Tool

Producers often look for ways to increase their income by introducing new crops or developing new livestock operations. Exogenous factors such as market forces, climate changes, and government policy provide impetus for change. In such cases, published budgets will assist producers in exploring new production possibilities. Budgets can help producers estimate potential costs and returns for new crops or livestock operations. For example, a producer with traditionally grown crops such as chile, cotton, wheat, or alfalfa may consider planting pecans on their farm. The investment will be huge, and before planting pecans, the producer should have a good idea about how much it will cost and what they might expect in terms of revenues. An enterprise pecan budget can help.

Evaluate Farm Performance

Using published enterprise budgets, producers can compare their farming performance to other producers in their county if the budgets with multiple producers’ performances are developed on average. New Mexico budgets have developed a “typical” operation with “above-average” management. They are not developed using averages, so producers need to be careful about comparing operations. However, U.S. Department of Agriculture budgets allow producers to look at averages. If producers find where they are performing, such as average, above, or below performance, then they have an opportunity to change their farming practices to achieve the best performance by reducing cost items and increasing their yields or find the best marketing route to give the best price of their products.

Data for Special Events

Budgets are also basic data sources for compensating producers’ incomes in case of special events, such as natural disasters, liquidating farms, or accidents. State governments, including the state legislature, lenders, insurance companies, real estate, bankers, and food processors, also find a need for crop and livestock budgets. These farm-supporting institutions benefit from the detailed knowledge of farm costs and returns so that producers know how they are doing in their business. For example, crop insurance is one of the important financial incomes to producers in case of natural disasters such as severe drought, flood, or wildfire. Crop insurance companies would pay accurate insurance premiums to producers when a natural disaster damaged a specific crop. Financial institutions and appraisers may be interested in budgets for compensation producers.

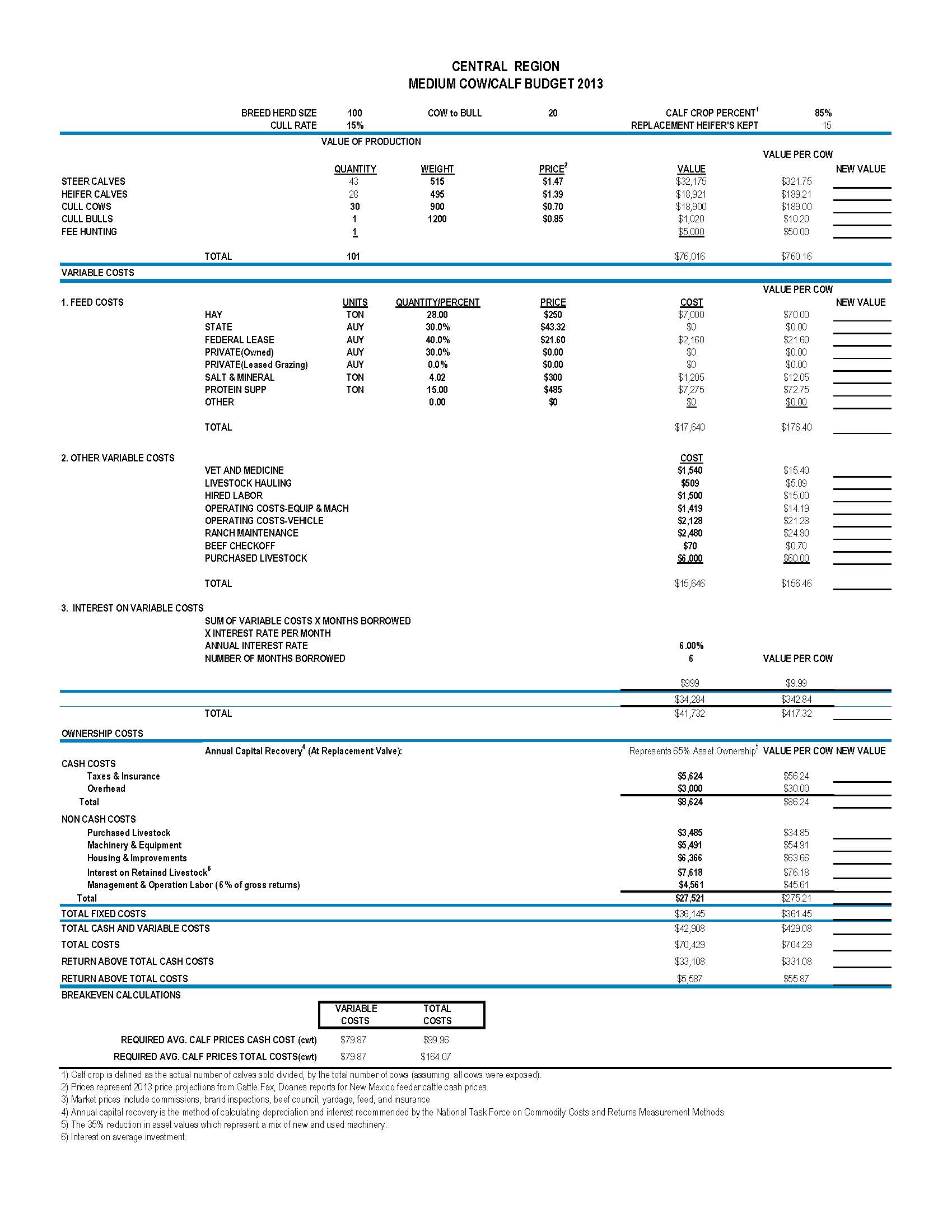

Example of Enterprise Budget

Appendix 1 presents an example of the published budgets developed by the NMSU Cooperative Extension Service. In part 2 of the series, we will explain how to interpret the budget items in the table.

If a producer wants to know about detailed enterprise budget information, please visit the website

https://costsandreturns.nmsu.edu

and should contact an enterprise budget specialist by emailing agcon@nums.edu phone or by calling 575-646-3215.

Appendix 1

REFERENCES

Chile Cost and Return Estimate, 2007, NM State University Cooperative Extension Service.

Lettuce Cost and Return Estimate, 2007, NM State University Cooperative Extension Service.

Onion Cost and Return Estimate, 2011, NM State University Cooperative Extension Service.

Range Livestock Costs and Returns for New Mexico, 2000, Range Improvement Task Force, NM State University Cooperative Extension Service.

The Handbook of Costs and Returns Analysis, American Agriculture Economic Association,

2001.

Budgets, New Mexico for crops and livestock, 2011-2022, at https://costsandreturns.nmsu.edu

AgEcon and AgBusiness Department History (1925-2012), NMSU Department of Agricultural

Economics and Agribusiness, 2013 at https://aeab.nmsu.edu/documents/2014updateforaeabhistory.pdf

Spanish version | Versión en español

Pilja Vitale is an extension economist in the Cooperative Extension Service at New Mexico State University. She received her B.S. in Agricultural Economics from Seoul National University, an M.S. in Agricultural Economics from Texas A&M University, and a Ph.D. in Agricultural Economics from Oklahoma State University. Vitale worked with vegetable farmers in Oklahoma for about 20 years and her interest areas are crop and livestock budgets and production economics.

Contents of publications may be freely reproduced, with an appropriate citation, for educational purposes. All other rights reserved. For permission to use publications for other purposes, contact pubs@nmsu.edu or the authors listed on the publication. New Mexico State University is an equal opportunity/affirmative action employer and educator. NMSU and the U.S. Department of Agriculture cooperating.

December 2023.