CR 595

Revised Fahzy Abdul-Rahman

College of Agricultural, Consumer and Environmental Sciences, New Mexico State University

Author: Extension Family Resource Management Specialist, Department of Extension Family and Consumer Sciences, New Mexico State University.

Introduction

Consumer credit, such as credit cards and loans, is a way of using future income to buy the goods and services you want today. When used wisely, credit can be a valuable financial tool. But when it is used carelessly, credit can cause serious financial problems.

Can you recognize the credit danger signals? Take a few minutes to consider these statements and check all that apply to you.

____ 1. I don’t save money.

____ 2. I’m always out of money before payday.

____ 3. I make new monthly credit card charges that are more than the monthly credit card payments I make.

____ 4. I need longer than the allotted time to pay an account balance.

____ 5. I juggle payments to creditors.

____ 6. I borrow to pay fixed expenses, such as insurance.

____ 7. I use credit card cash advances to pay everyday expenses.

____ 8. I receive calls and letters from creditors demanding payment of overdue bills.

____ 9. I’m unsure of how much I owe.

____ 10. I’m always late in paying my bills.

Now, total up the number of blanks you have checked. One check signals that you should use caution. Two checks mean that trouble is brewing. Three or more checks indicate that you should be very concerned and need to take some steps to help correct the problem.

Advantages/Disadvantages of Credit

Borrowing money isn’t good or bad in itself. It just depends on how you use it. When you use credit, you are actually paying to borrow someone else’s money. It’s up to you to pay back what you have borrowed by a certain date and at a specified cost to you, which is usually the amount borrowed plus interest charges.

Some advantages of using credit:

- Interest costs for some types of purchases may be deducted if you itemize deductions on your tax return. These include interest on a home mortgage, home equity loans, and some educational loans. Check with your tax preparer to see if any of these situations apply to you.

- When you repay a debt during inflationary times, you are actually repaying the debt with a lower dollar value than the one you borrowed on.

- It is possible to buy some goods at a lower price now than in the future.

- Credit cards are convenient to use and safer than carrying large amounts of cash.

- Credit allows you to buy items you can’t afford but need to pay for immediately.

- Some credit cards may have rewards, such as airline mileage, cash back, discounts, and gifts.

In desperate times, cash advance via credit cards may be affordable compared to predatory loans (such as payday loans, pawn shop, and car title loans), although cash advance is expensive due to high interest rates, upfront fees, and lack of grace period.

Some disadvantages of using credit:

- You may be easily tempted to buy more than you really need because it’s so simple to say, “Charge it.”

- Instead of comparison shopping for the best price, you may end up shopping at a store where you have credit.

- Buying on credit can be habit-forming and can add up to 20% or more to the cost of goods and services you purchase.

- If you do not repay quickly, you could actually end up paying more for an item you bought on sale than you would have paid at the regular price. Think about what you may have to give up later to pay for what you are getting now on credit. If you buy the stereo on credit now, what will you have to give up to repay the loan later? If you take out a student loan, will your increase in income cover the cost of repaying the loan? Is it worth it to use credit?

Credit is Not Free

Typical costs of credit or borrowing include the interest payment, periodic membership or annual fees, account set-up fees, application fees, late fees, balance transfer fees, and over-the limit fees. The cost of credit depends on whom you borrow from, your credit history, how much you borrow, and how long you take to repay the money you borrowed. Credit costs will vary from lender to lender. Before you borrow, compare the costs at several places. Use Worksheet 1 to compare rent-to-own, credit, and cash purchases. Annual percentage rate (APR) can be used to compare costs. The higher the APR and the longer it takes to repay the loan, the higher the total cost will be. At a given interest rate, borrowing a smaller amount of money will result in a lower overall credit cost to you. Therefore, a larger down payment will lower the total amount you will have to pay in interest charges.

The longer you take to repay your debt, the more you will pay. Don’t just look at how much you have to repay each month. Look at the total amount of money you will repay. Be sure you know the cost of credit. Try to take the shortest repayment period you can and make the highest monthly payments you can safely afford. Although repaying your debt in the shortest time will save money in interest charges, make sure that you have enough money to cover your current expenses as well. You do not want to create a situation in which you are stretching your cash flow too thin in order to repay a debt more quickly.

Credit Worthiness

Your credit history is based on your record of paying bills. It reflects your ability and willingness to repay debt in a prompt and reliable manner. A good credit history helps you qualify for future credit and may help you get credit at a lower cost. You can check your credit report through the three major credit-reporting services. Please refer to guide G-216, You Can Check Your Credit Rating (https://pubs.nmsu.edu/_g/G-216.pdf), for information on how to check your credit rating.

You should also know that insurance companies use credit histories to decide whether to cover you initially, to decide whether to renew your coverage, and to determine how much to charge you for coverage. Employers may use your credit history to check you out before you are hired or to decide whether to give you a promotion. Landlords also check it to decide whether or not to rent to you. Keeping a good credit history is important for all of these reasons.

Can I Afford It?

Let’s say you really want a new range for your kitchen, but you don’t have the money for it. What do you do? Do you borrow the money? Or do you wait until you can save some money and buy it later? Consider these basic guidelines when thinking about borrowing money.

- Needs vs. wants. Using the kitchen range example, first notice that it was worded as “you really want” and not “you need.” We are being targeted by advertisers and marketers to believe that the things we do not necessarily need are things that we can’t live without. Advertisements may persuade you to upgrade your adequate 2-year old cellphone to the latest high-tech $300 cellphone in order to keep up with the Joneses.

- Use the 15 to 20% rule. Your total debt load (except for your mortgage payment) should not exceed 15 to 20% of your monthly, after-tax income. Caution: This maximum may still be too high for some families, such as those with an uncertain job future, low income, high rent, or a high mortgage payment.

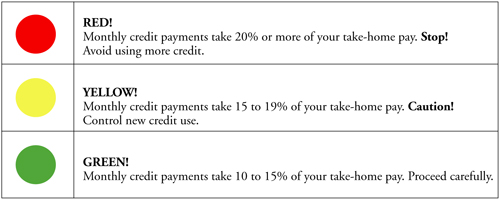

- Use the credit signal light from Worksheet 2 to help you. Write down how much money you bring home monthly. Multiply the amount by 0.20 for the maximum amount of credit you can afford. Compare this to your current monthly payments. Then decide if you can really afford to purchase that new range.

- How much credit you use is a personal decision, but look at your needs realistically. Credit is just one part of your spending plan. Consider carefully before committing any of your future income. If you promise all your money to credit repayment, you won’t have any money to live on.

Getting Out of Trouble

The best way to handle debts is to avoid them in the first place. However, we all know that avoiding debt is very difficult for the majority of families. If you checked two or more of the statements at the beginning of this publication, it’s time for you to act and do something to better manage your debt load.

(You can complete Worksheet 1 in Circular 592, Managing Your Money: Where Does All the Money Go? [https://pubs.nmsu.edu/_circulars/CR592.pdf], then use it with this publication to figure out how much you owe.)

- Make sure you know how much you owe and to whom. Use Worksheet 3 to list each creditor (loan company, bank, department store, or family member), the total balance owed, the date the monthly payment is due, the amount of the monthly payment, the number of payments left, and any amount that is past due. Total the balance owed. Next, total your monthly payments. Use Worksheet 4 to keep a record of when your payments are due each month.

- Look for ways to increase your income or decrease your spending. Try to free up some income so you can make your payments. You might want to re-read Circular 593, Managing Your Money: Stop Spending Leaks (https://pubs.nmsu.edu/_circulars/CR593.pdf), for tips on reducing your spending leaks.

- Do not use any more credit until you are in better financial shape. Try hiding those credit cards so you won’t be tempted to use them. You may even need to cut them up. That is exactly what some budget counselors make their clients do before payments are adjusted.

- If you know you will not be able to make your payments, contact your creditors. Do not ignore them. To be helpful, creditors must know of your problems before your payments are overdue. If you don’t contact them about your financial difficulties and don’t make scheduled payments, your account may be turned over to an independent collection agency. However, if creditors know the facts about your financial problems and are convinced of your intent to pay, many may agree to defer payments or refinance the debt to reduce the size of your monthly payments. Above all, be sure to keep your word. If creditors are willing to help you, be sure you follow through as you say you will. Only make promises that you are sure you will be able to keep.

- Obtain assistance from a credit counseling service. Contact the National Foundation for Credit Counseling (https://www.nfcc.org; 1-800-388-2227; Español 1-800-682-9832) for credit counselor listings in your area. Your county Extension office can provide budget counseling advice and information, but the staff is unable to mediate your payments with creditors.

Avoid Credit Card Blues

It is all too easy to make purchases when you just have to pull out the “plastic.” Easy, that is, until all of the monthly bills arrive. Many families use credit to make ends meet and then find it hard, if not impossible, to make all the monthly payments. That’s when the “credit card blues” set in. If you have trouble meeting your monthly payments, let it be a warning to you to cut back on credit use. If you have a hard time avoiding impulse buying, leave the credit cards at home.

Keeping track of what you charge will help keep you out of trouble. One suggestion to help you keep track is to use a separate check register to record credit card charges. Those purchases can add up at the end of the month.

Finding ways to reduce spending is hard for many families, but not impossible. Everyone in the family should be included in the cutbacks. The more involved family members are in planning ways to reduce spending, the more committed they will be to succeed. It also is a good lesson for your children to learn how to manage money responsibly early in life.

Conclusion: Be Credit Wise

- Credit can be a friend or a foe. It can be an asset or a liability. If you abuse the privilege, it can ruin future plans.

- Take some time to think before committing to additional debt and monthly payments. Consider the added cost that interest adds to your credit card payments and whether or not a product is worth the price of purchase.

- Decide how much credit you can afford and don’t exceed that amount.

- You have the responsibility to use credit wisely. If you find that your debts have piled up and are out of control, develop a plan to help solve the problem.

- Getting out of debt takes a lot of work and self-discipline. It can’t be done overnight, but it can be done.

Excel spreadsheet versions of some of these worksheets are available at https://pubs.nmsu.edu/_g/#circ.

Original author: Constance Kratzer, Extension Home Economist.

Fahzy Abdul-Rahman is the Extension Family Resource Management Specialist at New Mexico State University. He earned his Ph.D. and M.P.H. from The Ohio State University. His Extension programs focus on various personal finance topics, from basic banking to retirement planning.

Worksheet 1

Decisions, Decisions: Save First, Buy Later? Rent-to-Own? Buy on Credit?

John and Mary want to get a color television with a DVD player in time for Christmas. What should they do? Should they buy the TV on credit? Go to a rent-to-own store? Wait until next Christmas and save the money each week to pay cash for a new TV? First, they must decide if they have a real need for the television, or if they just want it.

Many people are attracted to rent-to-own stores because they can satisfy their wants immediately. If you are thinking about making a major purchase, weigh the pros and cons of each choice. Included here is a list of the options people have in making such a decision. Review them carefully so that when you are faced with this type of buying decision, you will be better prepared for the purchase. Table 1a is a sample comparison of a rent-to-own versus credit versus cash purchase. Use it as an example to fill in Table 1b for any major purchase.

Since rent-to-own stores have become very popular, here are some questions you will want to ask about their contracts before making a purchase.

- What is the total cost? Multiply the monthly payment amount by the total number of payments.

- Does the company guarantee that the item being rented is new?

- Can the item be bought outright at a reduced price at some point during the contract, or do you need to make all the payments to become the owner?

- Even though the company may provide repairs at no charge, does it also provide a substitute at no extra charge or stop payments during the repair period?

- Does the company require a large “balloon payment” at the end of the contract?

- If the renter misses one or more payments, can the contract be reinstated without the customer losing the investment up to that point? Are there costly penalties charged?

- Does the company require the renter to purchase insurance on the rented item, even if the customer already has home or renter’s insurance coverage?

Table 1a. An Example of Rent-to-Own Compared to Credit or Cash Purchase

| Rent-to-Own 78 weeks/18 months to ownership |

Credit Purchase 18 months |

Cash Purchase | |

| Cash price | — | $331.76 | $319.00 Price + 12.76 Sales tax $331.76 |

| Initial payment/down payment | First and last weeks’ payment = $22.88 |

10% down payment = $33 |

— |

| Installment payment | $11/wk + $0.44 tax = $49.19/mo1 |

$19.49/mo | — |

| Loan payments/down payment | $11.44 × 78 = $892.32 |

$19.49 × 18 = $350.82 + $33 down payment |

|

| Total cost | $892.32 | $383.82 | $331.76 |

| Extra $ (above the purchase price) | $560.56 | $52.11 | — |

| Effective APR2 | 163% | 21% | — |

| 1The weekly payment should be multiplied by 4.3 weeks in a month because assuming only 4 weeks per month would equal a 48-week year, hiding the cost of 4 weeks of payments. 2 The customer could not figure out the APRs without a special calculator, but comparing the relative total dollar costs is dramatic enough. Adapted from Senior Consumer ALERT, American Association of Retired Persons (1993). |

|||

Table 1b. Rent-to-Own Compared to Credit or Cash Purchase (Worksheet Download)

| Rent-to-Own 78 weeks/18 months to ownership |

Credit Purchase 18 months |

Cash Purchase | |

| Cash price | — | $ Price + Sales tax $ |

|

| Initial payment/down payment | First and last weeks’ payment = $________ |

% down payment = $________ |

— |

| Installment payment | $______ /wk + $______ tax = $______________ /mo1 |

$__________ /mo | — |

| Loan payments/down payment | $__________× = $ _________________ |

$__________× = $_______+ $ _______ |

|

| Total cost | $__________ | $________ | $__________ |

| Extra $ (above the purchase price) | $__________ | $__________ | — |

| Effective APR2 | % __________ | % __________ | — |

| 1The weekly payment should be multiplied by 4.3 weeks in a month because assuming only 4 weeks per month would equal a 48-week year, hiding the cost of 4 weeks of payments. 2 The customer could not figure out the APRs without a special calculator, but comparing the relative total dollar costs is dramatic enough. Adapted from Senior Consumer ALERT, American Association of Retired Persons (1993). |

|||

Worksheet 2

Credit Signal Light

Total monthly take-home pay = $ _____________________________

Total monthly non-mortgage debt owed = $ _____________________________

10% of take-home pay = $ _____________________________

20% of take-home pay = $ _____________________________

Compare your total monthly credit payment amount against your percentage of take-home pay.

Then follow the guidelines below.

Worksheet 3

How Much Do You Owe?

(Worksheet Download)

This worksheet will help you analyze your credit obligations. It is important for you to gather all of this information before you begin developing a money management plan. Do not include mortgage payments. Complete all the blanks that apply. Include all loans and credit cards.

| Company | Amount Still Owed |

Due Date | Monthly Payment |

Months Left to Pay |

*APR | Amount Past Due |

| E.g., Siti Credit Card |

$2,500 | 5th of each month |

$50 | 9 years (if minimum payment) |

14.99% | $877.20 |

| E.g., Seahorse Car Loan |

$3,200 | 7th of the month |

$400 | 8 | 4.5% | $0 |

| E.g., Holdit Pawn LLC |

$330 | In 25 days | — | — | 120% | — |

| Total Amount Still Owed: $ _______________ | ||||||

| *APR = Annual Percentage Rate Note: The average family should not commit more than 15 to 20% of its take-home pay to consumer debts. If your family is larger, you may need to keep the percentage even lower. To determine how much of your take-home pay goes toward consumer debt repayment, you need to calculate your Consumer Debt-Service Ratio. Consumer Debt-Service Ratio = Consumer debt repayment (monthly) / Take-home pay (monthly) |

||||||

Note: Consumer debt equals monthly repayments for all non-mortgage consumer debts, including home-equity credit-line loans. Take-home pay, sometimes called net pay or disposable income, is the income available after mandatory deductions for taxes and insurance. Irregular sources of earned or unearned income, such as interest earned or overtime earnings, are not included in disposable income for these calculations.

Worksheet 4

Income and Payment Calendar

(Worksheet Download)

Accountants may be the only ones who enjoy keeping records, but it's something you must do if you want to develop a workable money management plan. It doesn’t have to be a burden. Duplicate this calendar and use it each month, or just use your regular calendar. Fill in or highlight the dates you expect to receive income in

, the dates when bills are due in

, and other important information (e.g., CDs maturing, birthday expenses, etc.) in other colors. By using this system, you can see your finances in a specific time frame and plan ahead. The example below is for a month. You may simply have a list of items with their dates and expected income or payment. For example:

| No. | Item | Expected Date | Expected Income | Expected Payment |

| 1. | Tax refund | 02/28 | $2,500 | |

| 2. | Tuition fee, spring | 01/21 | $1,500 | |

| 3. | Car insurance | March & Oct. | $500/6 months | |

| 4. | Cellphone bill | Monthly | $55 | |

| 5. | ||||

| 6. |

You may also use an online calendar that is linked to your e-mail (e.g., Google Calendar) to have an e-mail reminder sent to you days, weeks, or even months before expected income or payment. A great advantage of this online calendar is its ability to have family members share these kinds of personal finance information so that even those without financial responsibilities will have a rough idea of the family’s cash flow.

| E.g.: Month, Year June, 2013 | ||||||

| Sunday | Monday | Tuesday | Wednesday | Thursday | Friday | Saturday |

| 1

Monthly

income from work |

2 | 3 | 4 | 5 | ||

| 6 | 7

Credit card

payments due |

8 | 9

Car

payment due |

10

Utilities

due |

11 | 12 |

| 13 | 14 | 15

Cellphone

payment due |

16 | 17 | 18 | 19 |

| 20 | 21 | 22 | 23 | 24 | 25 | 26

Expected

profit from garage sale |

|

27

|

28 | 29 | 30 | 31 | ||

| Month, Year | ||||||

| Sunday | Monday | Tuesday | Wednesday | Thursday | Friday | Saturday |

|

1

|

2 | 3 | 4 | 5 | ||

| 6 | 7 |

8

|

9 | 10 | 11 | 12 |

| 13 | 14 |

15

|

16 | 17 | 18 | 19 |

| 20 | 21 |

22

|

23 | 24 | 25 | 26 |

|

27

|

28 | 29 | 30 | 31 | ||

| Month, Year | ||||||

| Sunday | Monday | Tuesday | Wednesday | Thursday | Friday | Saturday |

|

1

|

2 | 3 | 4 | 5 | ||

| 6 | 7 |

8

|

9 | 10 | 11 | 12 |

| 13 | 14 |

15

|

16 | 17 | 18 | 19 |

| 20 | 21 |

22

|

23 | 24 | 25 | 26 |

|

27

|

28 | 29 | 30 | 31 | ||

To find more resources for your business, home, or family, visit the College of Agricultural, Consumer and Environmental Sciences on the World Wide Web at pubs.nmsu.edu.

Contents of publications may be freely reproduced for educational purposes. All other rights reserved. For permission to use publications for other purposes, contact pubs@nmsu.edu or the authors listed on the publication.

New Mexico State University is an equal opportunity/affirmative action employer and educator. NMSU and the U.S. Department of Agriculture cooperating.

Revised and electronically distributed on August 2012, Las Cruces, NM.